5 August 2024

Both the Fed and the Bank of England (BoE) did what markets expected at their latest policy meetings – the Fed standing pat and the BoE cutting by 0.25%.

The recent sharp recovery in the Japanese yen is a big development for markets. While the pace of the yen rally looks unsustainable, there are good reasons to expect further recovery in the coming months.

The Q2 earnings season continues in the US, and the broad picture so far is positive. Profits across the largest stocks are on course to grow at an annual rate of 10% this quarter. Further out, the consensus view is that there will be similar growth for the year as a whole.

From the aeroplane window, the ground below can look flat, at least until you start the descent. So it goes in investment markets in July – global stocks are little changed for the month. But, when you get closer, there has been a lot going on.

First, there has been the material correction in the US tech sector. The Philadelphia Semiconductor Index plunged -11% from its peak during the month, with the sell-off extending into August. And the closely-watched Magnificent Seven (Mag7) stocks slipped, with stretched valuations, uncertain profits guidance, and geopolitical tensions all bothering investors. That had consequences for tech-sensitive markets in Asia, too, with prices falling in Japan, Taiwan, and South Korea.

Second, while most momentum trades faltered (except India and gold), unloved value and small-cap stocks rallied. Other defensive sectors, like infrastructure and real estate, also benefitted. This rotation – a broadening of market performance – is a healthy development for the stock market. But it will need to keep going to cover the lost Mag7 index points.

Third, encouraging news on disinflation, a renewed prospect of interest rate cuts in H2, and the soft landing coming into view, suggest the sector rotation story can continue. Equally, the rally in US government bonds helps bolster equity risk premia across the board. And while tech valuations are stretched, they are not historically-extreme.

A number of developments are set to create a more volatile ride in markets during H2. Nominal growth is slowing, and could slow faster – something that has weighed on China’s stocks in July. Geopolitical stresses and US elections will matter too.

Securitised credit has been one of the best-performing areas of the fixed income universe over the past two years – and that’s expected to continue through 2024. Pivotal to its outperformance is that it’s a floating-rate asset class. That means income returns have been bolstered by higher central bank policy rates. Resilient economic conditions have played a part too, with falling spreads driven by robust credit fundamentals proving ideal conditions for capital growth.

Despite expectations of near-term US rate cuts – and the Fed easing could start from September – securitised credit should still hold appeal. Some investment specialists expect US policy to gradually shift towards a terminal rate of around 3.5%, a level where income from the asset class would remain high. Plus, there are added advantages for portfolios. Over the long term, securitised credit offers low correlation and low volatility versus other fixed income sub-asset classes. It also has a lower correlation to US equities than corporate bonds, making it an attractive diversifier for multi-asset investors.

The value of investments and any income from them can go down as well as up and investors may not get back the amount originally invested. Past performance does not predict future returns. The level of yield is not guaranteed and may rise or fall in the future.

This information shouldn't be considered as a recommendation to buy or sell specific sector/stocks mentioned. Any views expressed were held at the time of preparation and are subject to change without notice. While any forecast, projection or target where provided is indicative only and not guaranteed in any way.

Source: HSBC Asset Management. Macrobond, Bloomberg. See page 8 for details of asset class indices. Data as at 11.00am UK time 05 August 2024

Both the Fed and the Bank of England (BoE) did what markets expected at their latest policy meetings – the Fed standing pat and the BoE cutting by 0.25%.

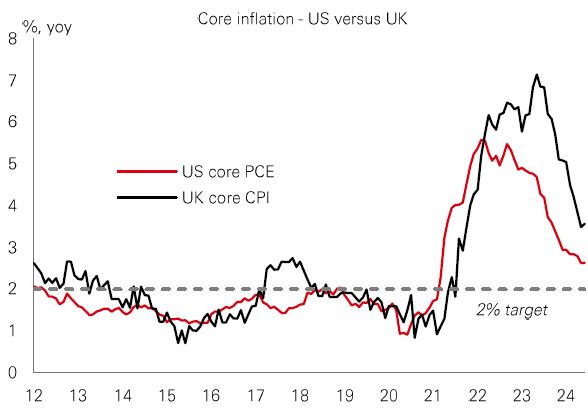

Core inflation is much closer to the target in the US than the UK and wage growth is more clearly moderating, which are consistent with a wide range of indicators showing that the US labour market is cooling. Moreover, the Fed has a dual mandate – inflation at target and full employment – whereas the BoE targets only inflation.

Looking ahead, the Fed may need to avoid further delaying rate cuts if it wants to secure the much talked of ‘soft-landing’. Gradual US slowdowns – such as those are seen at present – can morph into sharper slowdowns with little warning, and by that time, it is too late for policy makers to rescue the situation. The BoE, however, needs to stick to its guidance that it “will not cut rates too much or too quickly” given inflation is proving stickier in the UK than elsewhere.

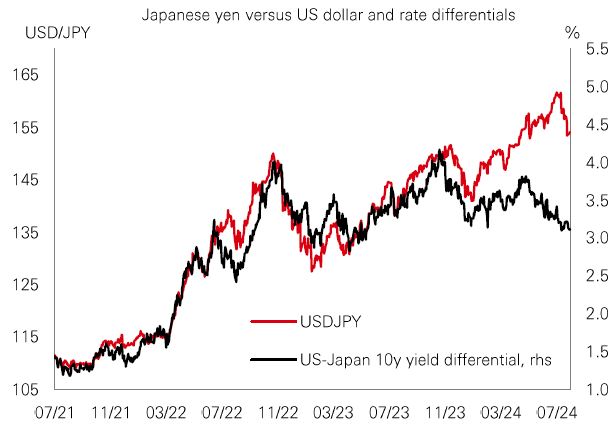

The recent sharp recovery in the Japanese yen is a big development for markets. The yen has been a major funding currency for carry strategies in recent years (where traders borrow yen to invest in higher-yielding currencies). But a strengthening yen – amid intervention by Japanese authorities – undermines the profitability of these trades, thus seeing them unwind. These carry trades may have also funded positions in other risk assets, possibly exacerbating the recent global tech sell-off. And a stronger yen potentially weakens domestic corporate profits, which is one reason why Japanese stocks sold off sharply last week.

While the pace of the yen rally looks unsustainable, there are good reasons to expect further recovery in the coming months.

The Bank of Japan’s gradual policy normalisation is important. But the more meaningful propulsion for the yen is likely to come from continued global disinflation. This could see interest rate differentials falling further in favour of the yen. 2024 promised to a be a good year for the yen – but maybe it’ll just be the second half?

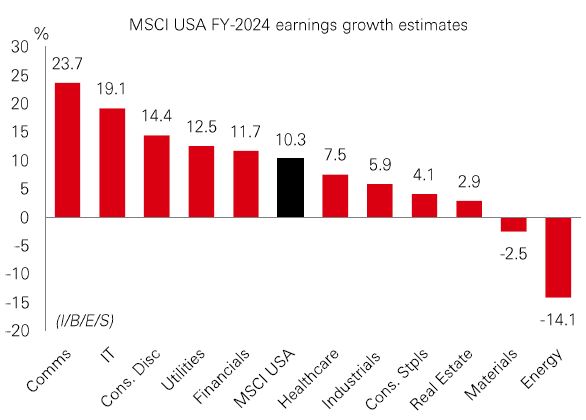

The Q2 earnings season continues in the US, and the broad picture so far is positive. Profits across the largest stocks are on course to grow at an annual rate of 10% this quarter. Further out, the consensus view is that there will be similar growth for the year as a whole. Those sectors reporting the strongest growth last quarter include communication services, IT, financials, and healthcare.

But there have been some disappointments. ‘Big tech’ sectors are set to drive the bulk of profits growth this year. Yet, stocks on high valuations – like many in the tech sector – have been battered on any hint that blistering profits growth is at risk. That’s extended to some Magnificent Seven stocks – which have wobbled at times.

More broadly, restrictive rates and signs of economic stress – particularly in the consumer sector – are causing pain in places. Consumer staples has been lacklustre in Q2, and when you adjust-out the influence of Mag7 stocks, the same goes for consumer discretionary, too. The cooling growth and weary consumers could pose a risk to profits in places near-term.

Past performance does not predict future returns. The views expressed above were held at the time of preparation and are subject to change without notice.

Source: HSBC Asset Management. Macrobond, Bloomberg, Datastream. Data as at 11.00am UK time 05 August 2024.

| Last week |

Source: HSBC Asset Management. Data as at 11.00am UK time 05 August 2024.

Global equities endured a sharp sell-off late in the week as markets digested disappointing economic data on US employment and manufacturing. It came after the Fed held rates steady ahead of expected policy easing from September, which triggered a fall in 10-year US Treasury yields. Mixed earnings news also played a part in the market-wide volatility, with ‘big tech’ stocks under pressure. Globally, the spillover was worst felt in Japan where the Nikkei 225 suffered a sharp reversal from recent all-time highs. Earlier last week, the Bank of Japan raised its policy rate to 0.25%. Elsewhere in Asia, India’s Sensex fell for the week, but China’s Shanghai Composite managed a modest gain. In commodities, the oil price was on course for its fourth consecutive weekly fall on signs of weak demand. Gold prices rebounded back towards record highs.

Note: Asset class performance on Page 1 is represented by the following indices:

US 60/40: Bloomberg EQ:FI 60:40 Index, Cash: JP Morgan Cash Index (3month), 10yr UST: ICE BofA 10yr US Treasury Index, Global Linkers: ICE BofAGlobal Inflation-Linked Government Index, Global IG: Bloomberg Barclays Global IG Total Return Index unhedged. Global High Yield Index: ICE BoFaUS High Yield Index, EMD Hard currency: US ABS: Bloomberg US ABS Floating Rate Total Return index; Bloomberg Barclays Global Aggregate Treasuries Total Return Index. EMD local currency JP Morgan EMBI Global Total Return local currency. Global Equities: MSCI ACWI Net Total Return USD Index. Value: MSCI Value Index, Growth: MSCI Growth Index, Global Emerging Market Equities: MSCI Emerging Market Net Total Return USD Index. China: MSCI China Index, India: MSCI India Index. Frontier: MSCI Frontier Markets Total Return Index, Alternatives: USD: DXY Index, Gold Spot $/OZ, Oil: WTI crude oil, Hedge funds: Credit Suisse Hedge Fund Index, Leverage Loans: JP Morgan liquid Loan Index, Infra Debt: iBoxx USD Infrastructure Total Return Index, Infra Equity: Dow Jones Brookfields Global Infrastructure Total Return Index, REITS Real Estate: FTSE EPRA/NAREIT Global Index TR USD. *Crypto: Bloomberg Galaxy Crypto Index.

Related Insights

As expected, the FOMC kept rates unchanged at the July meeting. The Fed funds rate remains...[1 Aug]

Despite media headlines about the US election, investors should focus on earnings, rates...[1 Aug]

Market expectations for Fed rate cuts have been on a roller-coaster ride, swinging from too...[23 May]

This document or video is prepared by The Hongkong and Shanghai Banking Corporation Limited (‘HBAP’), 1 Queen’s Road Central, Hong Kong. HBAP is incorporated in Hong Kong and is part of the HSBC Group. This document or video is distributed and/or made available by HSBC Bank Canada (including one or more of its subsidiaries HSBC Investment Funds (Canada) Inc. (“HIFC”), HSBC Private Investment Counsel (Canada) Inc. (“HPIC”) and HSBC InvestDirect division of HSBC Securities (Canada) Inc. (“HIDC”)), HSBC Bank (China) Company Limited, HSBC Continental Europe, HBAP, HSBC Bank (Singapore) Limited, HSBC Bank Middle East Limited (UAE), HSBC UK Bank Plc, HSBC Bank Malaysia Berhad (198401015221 (127776-V))/HSBC Amanah Malaysia Berhad (20080100642 1 (807705-X)), HSBC Bank (Taiwan) Limited, HSBC Bank plc, Jersey Branch, HSBC Bank plc, Guernsey Branch, HSBC Bank plc in the Isle of Man, HSBC Continental Europe, Greece, The Hongkong and Shanghai Banking Corporation Limited, India (HSBC India), HSBC Bank (Vietnam) Limited, PT Bank HSBC Indonesia (HBID), HSBC Bank (Uruguay) S.A. (HSBC Uruguay is authorised and oversought by Banco Central del Uruguay), HBAP Sri Lanka Branch, The Hongkong and Shanghai Banking Corporation Limited – Philippine Branch, and HSBC FinTech Services (Shanghai) Company Limited (collectively, the “Distributors”) to their respective clients. This document or video is for general circulation and information purposes only.

The contents of this document or video may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose. This document or video must not be distributed in any jurisdiction where its distribution is unlawful. All non-authorised reproduction or use of this document or video will be the responsibility of the user and may lead to legal proceedings. The material contained in this document or video is for general information purposes only and does not constitute investment research or advice or a recommendation to buy or sell investments. Some of the statements contained in this document or video may be considered forward looking statements which provide current expectations or forecasts of future events. Such forward looking statements are not guarantees of future performance or events and involve risks and uncertainties. Actual results may differ materially from those described in such forward-looking statements as a result of various factors. HBAP and the Distributors do not undertake any obligation to update the forward-looking statements contained herein, or to update the reasons why actual results could differ from those projected in the forward-looking statements. This document or video has no contractual value and is not by any means intended as a solicitation, nor a recommendation for the purchase or sale of any financial instrument in any jurisdiction in which such an offer is not lawful. The views and opinions expressed are based on the HSBC Global Investment Committee at the time of preparation, and are subject to change at any time. These views may not necessarily indicate HSBC Asset Management‘s current portfolios’ composition. Individual portfolios managed by HSBC Asset Management primarily reflect individual clients’ objectives, risk preferences, time horizon, and market liquidity.

The value of investments and the income from them can go down as well as up and investors may not get back the amount originally invested. Past performance contained in this document or video is not a reliable indicator of future performance whilst any forecasts, projections and simulations contained herein should not be relied upon as an indication of future results. Where overseas investments are held the rate of currency exchange may cause the value of such investments to go down as well as up. Investments in emerging markets are by their nature higher risk and potentially more volatile than those inherent in some established markets. Economies in emerging markets generally are heavily dependent upon international trade and, accordingly, have been and may continue to be affected adversely by trade barriers, exchange controls, managed adjustments in relative currency values and other protectionist measures imposed or negotiated by the countries with which they trade. These economies also have been and may continue to be affected adversely by economic conditions in the countries in which they trade. Investments are subject to market risks, read all investment related documents carefully.

This document or video provides a high level overview of the recent economic environment and has been prepared for information purposes only. The views presented are those of HBAP and are based on HBAP’s global views and may not necessarily align with the Distributors’ local views. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of its dissemination. It is not intended to provide and should not be relied on for accounting, legal or tax advice. Before you make any investment decision, you may wish to consult an independent financial adviser. In the event that you choose not to seek advice from a financial adviser, you should carefully consider whether the investment product is suitable for you. You are advised to obtain appropriate professional advice where necessary.

The accuracy and/or completeness of any third party information obtained from sources which we believe to be reliable might have not been independently verified, hence Customer must seek from several sources prior to making investment decision.

Important Information about HSBC Global Asset Management (Canada) Limited (“AMCA”)

HSBC Asset Management is a group of companies, including AMCA, that are engaged in investment advisory and fund management activities, which are ultimately owned by HSBC Holdings plc. AMCA is a wholly owned subsidiary of, but separate entity from, HSBC Bank Canada.

Important Information about HSBC Investment Funds (Canada) Inc. (“HIFC”)

HIFC is the principal distributor of the HSBC Mutual Funds and offers the HSBC Mutual Funds and/or the HSBC Pooled Funds through the HSBC World Selection® Portfolio service. HIFC is a subsidiary of AMCA, and indirect subsidiary of HSBC Bank Canada, and provides its products and services in all provinces of Canada except Prince Edward Island. Mutual fund investments are subject to risks. Please read the Fund Facts before investing.

®World Selection is a registered trademark of HSBC Group Management Services Limited.

Important Information about HSBC Private Investment Counsel (Canada) Inc. (“HPIC”)

HPIC is a direct subsidiary of HSBC Bank Canada and provides services in all provinces of Canada except Prince Edward Island. The Private Investment Counsel service is a discretionary portfolio management service offered by HPIC. Under this discretionary service, assets of participating clients will be invested by HPIC or its delegated portfolio manager, AMCA, in securities, including but not limited to, stocks, bonds, mutual funds, pooled funds and derivatives. The value of an investment in or purchased as part of the Private Investment Counsel service may change frequently and past performance may not be repeated.

Important Information about HSBC InvestDirect (“HIDC”)

HIDC is a division of HSBC Securities (Canada) Inc., a direct subsidiary of, but separate entity from, HSBC Bank Canada. HIDC is an order execution only service. HIDC will not conduct suitability assessments of client account holdings or of the orders submitted by clients or from anyone authorized to trade on the client’s behalf. Clients have the sole responsibility for their investment decisions and securities transactions.

Important Information about the Hongkong and Shanghai Banking Corporation Limited, India (“HSBC India”)

HSBC India is a branch of The Hongkong and Shanghai Banking Corporation Limited. HSBC India is a distributor of mutual funds and referrer of investment products from third party entities registered and regulated in India. HSBC India does not distribute investment products to those persons who are either the citizens or residents of United States of America (USA), Canada, Australia or New Zealand or any other jurisdiction where such distribution would be contrary to law or regulation.

The following statement is only applicable to HSBC Bank (Taiwan) Limited with regard to how the publication is distributed to its customers: HSBC Bank (Taiwan) Limited (“the Bank”) shall fulfill the fiduciary duty act as a reasonable person once in exercising offering/conducting ordinary care in offering trust services/ business. However, the Bank disclaims any guarantee on the management or operation performance of the trust business.

The following statement is only applicable to PT Bank HSBC Indonesia (“HBID”): PT Bank HSBC Indonesia (“HBID”) is licensed and supervised by Indonesia Financial Services Authority (“OJK”). Customer must understand that historical performance does not guarantee future performance. Investment product that are offered in HBID is third party products, HBID is a selling agent for third party product such as Mutual Fund and Bonds. HBID and HSBC Group (HSBC Holdings Plc and its subsidiaries and associates company or any of its branches) does not guarantee the underlying investment, principal or return on customer investment. Investment in Mutual Funds and Bonds is not covered by the deposit insurance program of the Indonesian Deposit Insurance Corporation (LPS).

THE CONTENTS OF THIS DOCUMENT OR VIDEO HAVE NOT BEEN REVIEWED BY ANY REGULATORY AUTHORITY IN HONG KONG OR ANY OTHER JURISDICTION.

YOU ARE ADVISED TO EXERCISE CAUTION IN RELATION TO THE INVESTMENT AND THIS DOCUMENT OR VIDEO. IF YOU ARE IN DOUBT ABOUT ANY OF THE CONTENTS OF THIS DOCUMENT OR VIDEO, YOU SHOULD OBTAIN INDEPENDENT PROFESSIONAL ADVICE.

© Copyright 2024. The Hongkong and Shanghai Banking Corporation Limited, ALL RIGHTS RESERVED.

No part of this document or video may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior written permission of The Hongkong and Shanghai Banking Corporation Limited.

Important information on sustainable investing

“Sustainable investments” include investment approaches or instruments which consider environmental, social, governance and/or other sustainability factors (collectively, “sustainability”) to varying degrees. Certain instruments we include within this category may be in the process of changing to deliver sustainability outcomes.

There is no guarantee that sustainable investments will produce returns similar to those which don’t consider these factors. Sustainable investments may diverge from traditional market benchmarks.

In addition, there is no standard definition of, or measurement criteria for sustainable investments, or the impact of sustainable investments (“sustainability impact”). Sustainable investment and sustainability impact measurement criteria are (a) highly subjective and (b) may vary significantly across and within sectors.

HSBC may rely on measurement criteria devised and/or reported by third party providers or issuers. HSBC does not always conduct its own specific due diligence in relation to measurement criteria. There is no guarantee: (a) that the nature of the sustainability impact or measurement criteria of an investment will be aligned with any particular investor’s sustainability goals; or (b) that the stated level or target level of sustainability impact will be achieved.

Sustainable investing is an evolving area and new regulations may come into effect which may affect how an investment is categorised or labelled. An investment which is considered to fulfil sustainable criteria today may not meet those criteria at some point in the future.